CYBERSECURITY RISKS AND MITIGATION

STRATEGIES IN THE INDIAN BANKING SECTOR

Namrata Verma 1![]()

![]() ,

Dr. Sanyam 2

,

Dr. Sanyam 2

1 Associate

Professor Psychology, Rajkiya Mahavidyalay

Modinagar, Ghaziabad, India

2 Assistant

Professor Cpommerce Rajkiya Mahila Mahavidyalaya

Nagla Kashi, Dhaulana, Hapur

|

|

|

ABSTRACT |

|

|

The

rapid-fire digitalization of fiscal services has significantly impacted the

global fiscal assiduity, particularly the banking assiduity, with significant

changes observed in the fiscal systems of arising husbandry similar as India.

Digital banking, mobile payment systems, and online fiscal services have

bettered the fiscal assiduity’s effectiveness and fiscal addition. still, the

increased use of digital structure has also redounded in exposure to a wide

range of cyber security pitfalls. Cyber security pitfalls similar as

phishing, ransomware, malware, bigwig attacks, and data breaches pose

significant pitfalls to the fiscal assiduity and its guests. The fiscal

assiduity of India has come a seductive target for cybercriminals because of

the increased digitalization of fiscal systems and the high volume of fiscal

deals reused on a diurnal base. This study aims to identify the primary cyber

security pitfalls faced by the fiscal assiduity of India and assess the

effectiveness of the cyber security mitigation strategies espoused by fiscal

institutions. The qualitative system has been used to conduct the study, and

secondary data has been used, which has been attained from the literature

review of colourful publications, reports, and

papers. The results attained indicate that cyber pitfalls in the fiscal

assiduity are rising with the increase in technology, cyberattack

methodologies, and the lack of cyber security mindfulness among the general

public. The results also indicate the part of technology, similar as artificial

intelligence, blockchain technology, and biometric technology, in perfecting

the cyber security of the fiscal assiduity. Eventually, the results attained

in the study are presented with suggestions and recommendations for the

development of an effective cyber security strategy, which can be used to

alleviate cyber security pitfalls and ensure the development of robust cyber

security systems to insure the trustability and responsibility of the digital

fiscal ecosystem of India. |

|||

|

Received 07 December 2024 Accepted 08 January 2025 Published 31 March 2025 Corresponding Author Namrata Verma, Namrata9476@gmail.com DOI 10.29121/granthaalayah.v13.i3.2025.6870 Funding: This research received no specific grant from any funding agency in

the public, commercial, or not-for-profit sectors. Copyright: © 2025 The Author(s). This work is licensed under a Creative Commons

Attribution 4.0 International License. With the license CC-BY, authors retain the copyright, allowing anyone

to download, reuse, re-print, modify, distribute, and/or copy their

contribution. The work must be properly attributed to its author.

|

|||

|

Keywords: Banking, Data Breach, Fiscal Ecosystem,

OTP and MFA |

|||

1. INTRODUCTION

The managing an account division plays a essential portion in supporting

productive development and monetary steadiness. In later times, innovative

development has essentially changed over the operations of keeping money

educate. The development of computerized managing an account administration,

counting web keeping money, versatile keeping money, and genuine- time

instalment frameworks, has upgraded accessibility, comfort, and adequacy for

visitors. India has persevered rapid-fire development in computerized financial

administrations over the once decade. Government venture pointed at advancing

advanced instalments and financial expansion have quickened the relinquishment

of electronic keeping money stages. The including infiltration of smartphones,

tall- speed web network, and monetary innovation comes about has assist

contributed to the development of computerized managing an account

administration. In spite of the multitudinous benefits of advanced

transformation, the developing dependence on advanced innovations has made

unused vulnerabilities in keeping money frameworks. financial educate store and

prepare huge volumes of touchy data, counting client individualities, financial

records, and deal information. In like manner, the keeping money division has

come a essential target for cybercriminals looking for

monetary pick up or key disengagement.

Cybersecurity pitfalls have come decreasingly

advanced and fragile to descry. Cyberattacks comparative as phishing cheats,

malware diseases, ransomware assaults, and information breaches can conceive

critical monetary misfortunes and harm the character of monetary teach. too,

cyber episodes may disturb keeping money operations and weaken open certainty

in computerized monetary administrations. The including complexity of cyber

pitfalls highlights the require for vigorous cybersecurity textures inside the

managing an account segment. Viable cybersecurity techniques bear a combination

of mechanical comes about, nonsupervisory oversight, danger operation hones,

and cybersecurity mindfulness among specialists and visitors.

This think about points to

look at the cybersecurity pitfalls confronted by the Indian managing an account

division and gauge relief procedures that can improve cyber flexibility. By

assaying being investigation and assiduity reports, the paper gives

perceptivity into the advancing cybersecurity topography and distinguishes

certain comes about for reinforcing keeping money security.

2. Problem

Statement

The fast extension of computerized keeping money

administrations in India has altogether expanded the introduction of money

related educate to cyber dangers. Whereas banks have received different

mechanical arrangements to move forward operational proficiency, numerous teach

still confront challenges in actualizing comprehensive cybersecurity

frameworks.

Cyberattacks focusing on keeping money frameworks

have gotten to be more visit and advanced, posturing genuine dangers to money

related soundness, client security, and regulation notoriety.

Despite executive trials and innovative marches,

multitudinous banks do to battle with cybersecurity vulnerabilities.

Subsequently, there is a require to methodicallly

look at the cybersecurity dangers influencing the Indian managing an account

division and assess compelling relief strategies.

3. Literature

Review

3.1. Cybersecurity in Monetary Systems

Cybersecurity alludes to the assurance of computer

frameworks, systems, and advanced data from cyber dangers and unauthorized get

to. Agreeing to Anderson

et al. (2019), cybercrime has gotten

to be one of the most noteworthy dangers confronting advanced budgetary

frameworks. The expanding reliance on computerized framework has extended the

assault surface for cybercriminals.

Financial educate are especially helpless to

cyberattacks since they oversee important budgetary resources and touchy

information.

3.2. Computerized Managing an account and Cyber Risk

The computerized change of money related

administrations has presented various mechanical advancements in the keeping

money segment. Arner et

al. (2017) contend that fintech

advancements have altogether progressed popular consideration and functional

proficiency. In addition, these advances have also posed a number of

cybersecurity challenges.

The integration of protean keeping plutocrat

operations, pall computing stages, and third- party plutocrat related

administrations has expanded the complexity of keeping plutocrat fabrics and

extended implicit section focuses for cyberattacks.

3.3. Common Cyber risks in Banking

Research thinks about recognize a few major cyber

dangers influencing the keeping money segment. Phishing assaults are among the

most common troubles, as cybercriminals use deceiving communication strategies

to get secret data from guests Hadnagy

(2018).

Malware assaults and ransomware occurrences are

moreover predominant dangers that can compromise managing an account framework

and disturb money related operations. Agreeing to Romanosky

(2016), ransomware assaults

have expanded essentially in later a long time, especially in businesses taking

care of delicate budgetary information.

Table-1

|

Table 1 Major cybersecurity Threats in

Banking Sector in India |

||

|

Cyber Threatt |

Description of Cyber Threat |

Impact on Banking System |

|

Phishing |

Fraudulent E-Mail or messages are used to steal

login credentials |

Unauthorised account access |

|

Malware |

Malicious software is installed that infiltrates

the banking system |

System is compromised and data theft |

|

Ransomware |

Data is encrypted and ransom demand |

Operational disruption |

|

Data Vulnerability |

weakness in system, software or human processes |

unauthorised access to sensitive information of

individual or corporate |

|

Insider Threat |

Authorised access is misused by employees |

Data leaks and financial frauds |

|

Sim Swapping |

Mobile number is fraudulently transferred to

attackers |

OTP interception and account is takeover by

attackers |

4. Research

Methodology

4.1. Research Design

The study is based on qualitative research design

so as to analyse the cybersecurity risk and mitigation strategies in the

banking sector of India. The qualitative approach allows an in-depth

examination of cybersecurity challenges and solutions on the bases of existing

literature and industry data.

4.2. Data Collection

The secondary data was used in the study which

collected from-

·

Academic Journals accompanying cybersecurity,

FinTech and Digital Banking System

·

Government reports on banking

·

Industrial publication

4.3. Objectives of Study

·

To Identify and analyse major types of cyber

risks faced by banks

·

To suggest suitable strategies and best

practices for strengthening cyber risk management

5. Risk of

Cyber Security in Indian Banking System

5.1. Phishing and Social Engineering

It is an attempt to pilfer sensitive information

of customer by pretending to be trustworthy. The customer might get an E-Mail

that looks like it is from the bank or customer may get a text message saying

his delivery needs confirmation. it looks like normal but behind it is a

fraudster. Without social engineering phishing is not possible to be succeed

its helps to understand how individuals respond under pressure. Psychology is

more often used by attackers than technology.

Phishing isn't just one method instead takes many

forms-

·

E-Mails containing fake links

·

Text messages containing links to harmful

websites

·

Phone calls in which the caller claims to be an

official

·

Social media chats asking for personal

information

Preventions strategies from phishing attacks

·

Anti-phishing plug-ins can be used that warn

before clicking a harmful link

·

E-Mail gateways can be used so as to filter

suspicious content

·

Training Programs can be organised that simulate

phishing attacks to prepare employees

5.2. Malware and Banking Trojans

Malware is malicious software that is designed to

disrupt, damage or steal sensitive information from user's device. Banking

trojans is also a malware that is specially designed to target online banking

platforms and capture login credentials, debit card/credit card information One

Time Passwords (OTP) and Multi Factor Authentication (MFA) codes, session data

and device fingerprints etc. Banking trojans target those users and

organisations that regularly access financial services online. The common banking

trojans are- Zeus(Zbot), TrickBot, Emotet, Dridex and Mobile banking trojans.

Preventions Strategies from Malware and banking

trojans-

An individual can prevent himself from malware and

banking trojans by avoiding phishing, keeping software update, using security

tools, by enabling MFA code and regularly monitoring accounts.

5.3. Ransomware Attacks

With over 10% of all the data breeches, ransomware

attacks are currently third most popular type of malware. It is type of malware

which is used as a tool to pilfer sensitive information and essentially hold it

hostage. the data is only released after cyberattackers

get ransom payment. Once the ransomware enters into the computer it infects it

covertly. The software then attacks files and accesses and modifies the

credentials. Consequently, the person who control the malware holds hostage the

computer infrastructure.

Preventions Strategies from Ransomware Attacks

Ransomware attacks can be prevented by-

·

Keeping devices updated

·

Always install software from trusted and

verified sources

·

Installation of antivirus protection in devices

·

Always have Back-Up of data

·

Provide training employees

5.4. Data Vulnerability

Data vulnerability is a weakness in system,

software or human processes like unpatched software, use of weak passwords or

phishing. Data vulnerability allows unauthorised access to sensitive

information of individual or corporate.

Preventions Strategies from Data Vulnerability

preventions can be used-

·

keep updated software regularly

·

Use of strong passwords and MFA

·

Provide training to employees

·

Limit access user and permissions

5.5. Internal Threats

Every organisation has people who have authorised

access to its system and network these people might be present employees,

former staff, consultants, board members or business partners. An insider

threat occurs when someone having authorised access uses it to compromise the

organisation's cybersecurity intentionally or unintentionally. Insider threats

are intentional, unintentional, collusive threats, third party threats and

malicious threats.

Preventions Strategies from Insider threats-

·

Access control and least privilege

·

Implementation of regular monitoring and

auditing of user activities

·

Deployment of data loss prevention (DLP) tools

6. Data

Analysis and Results

The incidents of cybercrime in India have

increased significantly in the past decade which is due the rapid expansion of

digital banking platforms, Mobile payment system and online financial services.

As the digital transactions are increasing the cyber criminals are getting more

opportunities to take the advantage of loopholes of financial systems. As per

the NCRB data 2023-25, India experienced a 31% jump in cybercrimes with over

86000 cases reported.

Table 2

|

Table 2 Cybercrime and Financial Fraud

Cases in India |

|||

|

Year |

Reported Cybercrime Case |

Financial Fraud Cases |

Estimated financial Loss (in ₹ Crore) |

|

2019 |

44546 |

12317 |

1246 |

|

2020 |

50035 |

14678 |

1903 |

|

2021 |

52974 |

16112 |

2150 |

|

2022 |

65893 |

18902 |

2750 |

|

2023 |

71468 |

21349 |

3450 |

|

2024 |

80000+ |

25000+ |

4000+ |

|

Estimated are Based on the Cybersecurity

Industry Reports. Source:

NCRB, Cybersecurity Reports by RBI and Cybersecurity Industry Analysis |

|||

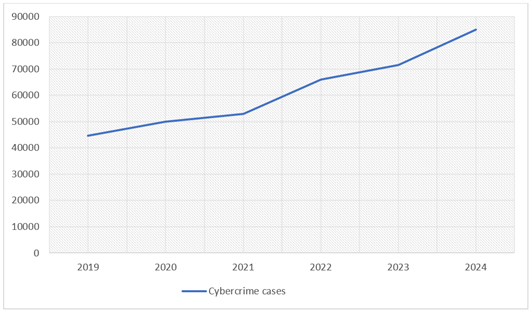

Figure 1

|

Figure 1 Cybercrime Cases |

From the above table and figure it is clear that

reported cybercrimes and financial fraud have grown steadily each year.

Cybercrime attacks have increased by nearly 80% from 2019 to 2024. This increase reflects the rapid adoption of

digital technology and increased use of online platforms, mobile banking and

digital payments. Financial fraud cases have also risen sharply, from 12317 in

2019 to more than 25000 in 2024. This increase suggests that cybercriminals are

increasingly targeting financial transactions and services and exploiting

vulnerabilities in banking and payment system. The financial losses from

cybercrime have also increased significantly, from ₹1246 crore in 2019 to

an estimated ₹4000 crore in 2024. This increase shows that cybercrimes

are not only increasing in volume but their impact and consequences are also

becoming more severe.

7. Conclusion

In conclusion it is clear that cyber threats to

India's digital economy are rapidly increasing. This situation underscores the

need for robust cybersecurity measures, stricter regulatory laws, and increased

awareness among users and organizations. The rise in financial fraud cases, in

particular, indicates that cybercriminals are increasingly focusing on

financial systems, requiring the banking and financial sector to strengthen its

security. The findings of the study indicates that cybersecuirty

has become a critical part of modern banking operations. As cyber threats

evolve, financial institutions must adopt proactive and adaptive security

strategies. One of the most effective methods of preventing from cyber risk is

to implement a multi-layered security architecture that integrates multiple

defence mechanisms. These may include firewalls, encryption protocols,

intrusion detection system and authentication techniques.

In

addition, cybersecurity strategies must also address human factors. Employee

training and customer awareness programs are crucial to mitigating

vulnerabilities associated with phishing attacks and social engineering.

CONFLICT OF INTERESTS

None.

ACKNOWLEDGMENTS

None.

REFERENCES

Anderson, R., Barton, C.,

Böhme, R., Clayton, R., van Eeten, M. J. G., Levi, M., Moore, T., and Savage,

S. (2019). Measuring the

Cost of Cybercrime. Journal of Cybersecurity, 5(1),

1–19.

Arner, D. W., Barberis, J. N., and Buckley, R. P. (2017).

FinTech and the Transformation of Financial Services. Journal of Banking Regulation, 19(3), 1–17.

Hadnagy, C. (2018). Social Engineering: The

Science of Human Hacking. Wiley. https://doi.org/10.1002/9781119433729

Kshetri, N. (2020). Cybersecurity

in the Financial Services Industry. Computer, 53(2),

16–24.

Reserve Bank of India. (2021). Cyber Security Framework for Banks. RBI Publications.

Romanosky, S. (2016). Examining the Costs

and Causes of Cyber Incidents. Journal of Cybersecurity, 2(2), 121–135.

https://doi.org/10.1093/cybsec/tyw001

World Economic

Forum. (2020). Global Risk Report. World Economic Forum.

This work is licensed under a: Creative Commons Attribution 4.0 International License

This work is licensed under a: Creative Commons Attribution 4.0 International License

© Granthaalayah 2014-2025. All Rights Reserved.