ShodhKosh: Journal of Visual and Performing ArtsISSN (Online): 2582-7472

|

|

Digital Transactions and Cultural Participation: Factors Influencing Mobile Payment Adoption Among Older Adults

Asmita 1![]()

![]() ,

Dr. Jayaashish Sethi 2

,

Dr. Jayaashish Sethi 2![]()

![]() ,

Dr. Sarishti Joshi 3

,

Dr. Sarishti Joshi 3![]()

![]() ,

Trinkul Kalita 4

,

Trinkul Kalita 4![]()

![]() ,

Dr. Jayanthi Rajendran 5

,

Dr. Jayanthi Rajendran 5![]()

![]() ,

Mandeep Kaur 6

,

Mandeep Kaur 6![]()

![]()

1 Research

Scholar, Maharishi Markandeshwar University (Deemed to be University), Mullana,

India

2 Professor,

Maharishi Markandeshwar University (Deemed to be University), Mullana–Ambala, India

3 Assistant Professor, Faculty of Liberal Arts, The ICFAI University, Baddi, Himachal Pradesh, India

4 Assistant Professor, Assam Down Town University, India

5 Associate Professor and Head, Department of English, Easwari

Engineering College, Chennai, India

6 Assistant Professor, Department of

English Language, Guru Nanak Dev University, Amritsar – 143005, India

|

|

|

ABSTRACT |

|

|

The rapid

expansion of digital payment technologies has significantly reshaped modes of

exchange across sectors, including the cultural and creative economy. Despite

widespread diffusion of mobile payment systems, adoption among older adults

remains comparatively limited, potentially influencing their participation in

digitally mediated cultural activities such as online ticketing, event

access, and heritage engagement. Understanding the behavioural and

psychological drivers of mobile payment usage within this demographic is

therefore essential for fostering inclusive digital ecosystems. This study

investigates the determinants of mobile payment adoption among adults aged 55

years and above by extending the Technology Acceptance Model (TAM) with

constructs of trust and multidimensional perceived risk. Data were collected

through a standardized questionnaire administered to 326 older adults in the

Delhi NCR region. Structural Equation Modelling (SEM) was employed to test

the proposed relationships. Findings confirm that perceived ease of use and

perceived usefulness significantly shape attitudes toward mobile payment

technologies, supporting the explanatory power of TAM in later-life

technology adoption. Trust emerges as a central mediating mechanism, enhancing

perceived usefulness and positively influencing attitudes while mitigating

the negative effects of perceived risks. Among risk dimensions, performance

risk and financial risk exerted the strongest influence on trust, whereas

psychological, privacy, and time risks demonstrated comparatively weaker

effects. Attitude toward mobile payment systems was identified as the most

significant predictor of behavioural intention, highlighting the importance

of positive experiential and cognitive evaluations. By situating mobile

payment adoption within the broader context of digital access and

participation, this study contributes to discussions on digital inclusion,

user experience, and accessibility for older populations. The findings hold

implications for designers, cultural institutions, and policymakers seeking

to enhance older adults’ engagement with digitally enabled services and

cultural platforms. |

|||

|

Received 21 September 2025 Accepted 25 December

2025 Published 17 February 2026 Corresponding Author Asmita, Asmitaahuja29june@gmail.com DOI 10.29121/shodhkosh.v7.i1s.2026.7175 Funding: This research

received no specific grant from any funding agency in the public, commercial,

or not-for-profit sectors. Copyright: © 2026 The

Author(s). This work is licensed under a Creative Commons

Attribution 4.0 International License. With the

license CC-BY, authors retain the copyright, allowing anyone to download,

reuse, re-print, modify, distribute, and/or copy their contribution. The work

must be properly attributed to its author.

|

|||

|

Keywords: Mobile Payment Adoption, Older Adults, Digital

Inclusion, Trust and Risk Perception, User Experience, Cultural

Participation, Technology Acceptance |

|||

1. INTRODUCTION

The explosion of

mobile payment (m-payments) technologies have changed the way finances are

managed along with providing convenience, speed and accessibility. The use rate

of mobile payment is getting more popular in the world, and it is mixed in

people's daily life. Also, older age has a relatively slow adoption of ads

which is due to the inherent technological ineptitude of this population, in

comparison to younger ages Chawla

and Joshi (2019). The adoption digital divide has attracted

much attention from academics and policymakers who endeavour to reduce the

digital divide and improve financial inclusion among the older demographic

group. Senior and older people have particular challenges associated with using

mobile payment systems. The issues are physical, cognitive and psychological

obstacles, security, trust and privacy Hoque and

Sorwar (2017). Based on rapid technology development and worsened by the

COVID-19 epidemic, several factors affecting acceptance of mobile payment have

been highlighted as a major concern among elderly to encourage their adoption Bruine

and Bennett (2020), Zhao and Bacao (2021). The use of mobile payment has the

potential to have significant impact on their financial independence, social

inclusion and access to basic services, and is therefore an important area to

study.

The Technology

adoption behavior has been studied well through the use of different

theoretical models including the Technology Acceptance Model (TAM) and its

extensions, like Unified Technology Acceptance and Use Theory (UTAUT), and the

UTAUT2 model Venkatesh

et al. (2003), Venkatesh and

Bala (2008). These models describe antecedents of individual new

technology acceptance behaviour, and include perceived usefulness, perceived

ease of use, social influence, and enabling environments. Mobile payments have

led to the study of the factors that affect acceptance of mobile payment as

being trust and risk and ease of use of the technology Albashrawi

and Motiwalla (2019), Kim et al. (2019).

In the case of older adults, many variations of these models have been

suggested in order to better represent the specific features and challenges

that this population is facing. The perceived psychological risk and trust

construct of mobile payment adoption are better for the older generation than

the younger generation, that has the tendency toward adopting new technologies Khasawneh and Irshaidat, (2017), Hanif and Lallie (2021). Furthermore, as the older

adults are willing to make a decision related to technology adoption with the

opinions of external parties, this study found that subjective norm and social

influence were anticipated to be significant predictors of mobile payment

adoption among older adults Cham et al. (2021).

The risk

perception of mobile payment is a significant factor in keeping the senior

citizens from accepting mobile payments. Perceived performance risk, financial

risk and privacy risk are prominent issues for older users Johnson et al. (2018). Due to lower entry

barriers, perceived financial and psychological risks perceived by this

demographic group are higher than institutional investees of a higher age

although they may have lower exposure to digital technologies and be more

vulnerable to fraud Khalilzadeh et al. (2017).

Furthermore, trust is an important ingredient for mobile payment as users have

to reveal sensitive financial information in the process of a transaction. In

the case of older people in particular, consumer intent could be heavily

determined by whether they trust the technology, who provides the mobile

payment service and the security of the transaction (Auer et al. 2020, Bhatt

and Mehta (2020). Trust is found to be a key determinant in

the technology adoption cycle, and multiple studies have indicated that the

older generation is more reluctant to adopt mobile payment due to privacy and

security concerns Sleiman

et al. (2022). A few recent studies show that trust in

technology and payment system can mitigate the impact of perceived risks Tandon et al. (2018). Social support from family

and friends has a very positive impact on their perception of risk and belief

in the technology, which is more important for the older users Saha and Kiran (2022).

Perceived

usefulness and perceived ease of use are two of the most significant factors to

mobile payment adoption and have always been the key to the TAM and UTAUT

models Darma

and Noviana (2020), Ghilarducci

(2022). Older people will adopt mobile payments

from the personal usefulness of the technology, which encompasses access to

financial services, and being able to avoid carrying money Zhao and Bacao (2020). This latter factor is especially relevant

for older persons who may not be digital natives and may, therefore, have

cognitive or physical challenges accounting for their use of they interact with

digital interfaces Hoque and Sorwar (2017).

Recent research found there is a higher likelihood that older men adopt mobile

payments if the mobile payment interface is intuitive and requires less

learning or alteration Lin et al. (2018).

Therefore, mobile payment providers must have the platform become intuitive, accessible

and easy to use for this group of the population Sleiman

et al. (2022).

Attitude refers to the positive or negative feelings a

person has towards the use of a particular technology, and they are greatly

influenced by the utility, ease of use and associated risks of the technology Li et al. (2020). Numerous studies show that older

persons have primarily negative views towards m-payments in contrast with

younger users, mainly because of concerns over security, ease of use and

complexity of the technology Berg and Liljedal (2022), Sun et al. (2020).

Increased trust between older persons in security and privacy issues of mobile

payments is associated with more positive sentiments and therefore enhances

their intention to use the technology Wong and Mohamed (2021). The informing of the

subjective norms goes a long way in influencing the behaviour of the senior

citizen, where the influence of the family members, caregivers and peers

influences their behavioural attitudes and intentions regarding the adoption of

mobile payments Scherer and Teo (2019).

It is important to the society to know the factors related

to the adoption of mobile payments among the old people, especially the

relationship with digital literacy and financial inclusion. With the growing

popularity use of mobile payments, older persons who do not use these

technologies could lose more margin in society Scherer

and Teo (2019). This research will result in research knowledge on

exploring perceived dangers, trust, ease of use and social factors affecting

acceptance of mobile payments among the older persons and develop more

accessible and user-friendly mobile payment systems among the older persons.

The research findings will contribute to policy makers and enterprises'

awareness of the barriers to adoption and should lead to initiation-specific

measures to compensate for certain challenges encountered by older people for

mobile payment applications. This may include activities such as raising

awareness campaigns, employing easier payment mechanisms and better security

controls which are more optimal for older users Sleiman

et al. (2022).

Furthermore, the knowledge about the role of attitude and behavioural intention

in the adoption process is valuable in understanding how the older person

arrives at decisions on adoption of technologies and which areas are the focus

in order to provide good rates of adoption.

Older persons' acceptance of mobile payment technology is

influenced by a complex interaction of subjective risk, trust, perceived

usefulness and social factors. In spite of many benefits of mobile payments in

terms of convenience and availability, elderly people share unique challenges

that hinder them from popular adoption of these technologies. Thus, this

research attempts to explore factors associated with mobile payments adoption

among elderly persons based on the established technology acceptance model

(primarily TAM and UTAUT), and assess the effects of barriers, trust and

attitudes on adoption intentions. These aspects will be narrated in this

research work, seeking to build beneficial knowledge about how the adoption

process occurs in older adults, and in order to present a proposal concerning

how to enhance financial inclusion and digital literacy among the population.

2. Theoretical Foundation

This research

applied the TAM and UTAUT models to analyse the determinant on the acceptance

of mobile payment by senior citizens for the general understanding of the

adoption of new technologies based on a range of perceived attributes such as

usefulness, ease of use and social impact on society Hoque

and Sorwar (2017). The TAM model, proposed by Davis

(1989), states that perceived usefulness and ease of use are the two

main factors that affect technology acceptance. PU means the perception of old

people for mobile payments, ease to manage their money and daily activities,

whereas PEOU can be stated as a degree of ease of use of the mobile payment

technology and could have a great impact on the adoption choice of the older

person Albashrawi

and Motiwalla (2019). These variables are developed further and

improved by the UTAUT model, which improves TAM by adding the importance of

social influence, enabling factors and performance expectancy associated with

the decisions to use technologies Olsson et al. (2019).

Norms, in other words, subjective social pressure to use or not to use mobile

payments is important for older people Cham et al. (2021).

Moreover, trust in security and privacy of mobile payment systems is vital in

the case of the behaviour of senior users while it comes to these Khalilzadeh et al (2017). This study abbreviates

the use of the Perceived Risk model, which lays an emphasize on the emotional

and financial risks that older persons associate with the use of mobile

payments Scherer and Teo (2019). The

perceived risks of privacy and performance combine to lead to lack of trust and

consequent lack of adoption for older demographics who can already be feeling

vulnerable to fraud Wong and Mohamed (2021). These theoretical frameworks present a strong foundation for

investigating mobile payment acceptance among older persons, which includes the

dynamics of usability, trust, social impact and perceived dangers Sundararajan and Muhammed (2024).

3. Review of Literature

Mobile payment (m-payment) technology has the potential to revolutionise the financial systems of the world, enabling the ease and effectiveness of making digital transactions, and encouraging financial inclusion Bailey et al. (2017), Lee and Shin (2018), and has experienced tremendous growth recently. Despite these benefits, however, the uptake of mobile payments among older persons is still low despite different factors driving older adults' behaviour, psychology, and context Choudrie et al. (2018), Berg and Liljedal (2022). Moreover, the older consumers have been found to have greater technology resistance, cognitive barrier and greater sensitivity to uncertainty which highlight the importance to explore the perceived risk variable affecting the confidence in mobile payment system Hoque and Sorwar (2017), Olsson et al. (2019). For example, trust (i.e. confidence in reliability and integrity) is the most important factor that determine acceptability of digital banking by older people Talwar et al. (2020), Wong and Mohamed (2021). While multiple studies have been proven with various contexts of payment systems, trust has been consistently mentioned as one of the antecedents affecting risk perceptions, anxiety and behavior Johnson et al. (2018).

3.1. Perceived Performance Risk AND Trust

Perceived

Performance Risk is about safety risk which deals with doubts about the

effectivenessness, reliability and stability of systems Zhao and Bacao (2020). Senior people often question the

accountability of m-payment services in having errorless transactions and

consistency in the service, and this leads to the withdrawal of engagement with

the technology or the use of conventional payment services. Research shows that

failure in performance has a negative effect on user (Marriott & Williams)

confidence, and results in inconsistency in engagement Choi

and Choi (2017). A study of digital banking and mobile retail found low

ambiguity in functionality had a significant impact in reducing the

determination of building trust and adopting or not Makanyeza

(2017), George

and Sunny. (2021). Furthermore, elderly users are a

vulnerable group of high-risk payers, and have a lower threshold for

transactional errors, and they are more likely to blame themselves for trying

to use the platform, as they are more likely to attribute the failure of the

platform to built-in structural flaws Scherer and

Teo (2019), Mutimukwe et al. (2020).

Besides, system credibility and service reliability is weakened due to

perceived instability of the system technology Patil

et al., (2020), Kuo (2020).

Performance risk is also further increased with older consumers having low

levels of technical knowledge on troubleshooting or solving digital issues,

thus undermining their trust in MPPs Singh

and Srivastava (2020), Tripathi

et al. (2022).

3.2. Financial Perceptions of Risk and Trust

Financial Risk is

the fear of losing money due to fraud, unauthorised transactions, technical

failure or hidden fees Ozturk et al. (2017),

Widyanto

et al. (2022). Senior citizens have a higher perception

of their risk of being a victim of online fraud because they have less

cybersecurity knowledge and are more prudent with their money Li et al. (2020), Abegao

et al. (2022). A consensus is on point in the literature

viewed as the lower level of trust in the fintech platforms for this situation:

perceived financial risk reduces transaction confidence and weakens trust in

the fintech platforms Johnson et al. (2018),

Bashir et al. (2018). In fact, the direct

link between m-payment operations and banking and individual finances is what

makes older individuals more financially anxious Sobti

(2019), Santosa et al.

(2021). It is evident that distrust of financial systems is impeding

technology-mediated transactions in the context of low levels of digital

ecosystem maturity Loh et al. (2020), Sleiman

et al. (2022). Moreover, elderly people with a high

priority on financial security and stability, making associations with

financial loss; using digital payments results in reduced trust in and

motivation toward adopting mobile payment Darma

and Noviana (2020), Fan et al. (2022).

3.3. Time Risk Perception and Trust

Time perception

risk is the perception that it may take more time and cognition to introduce

and manage new payment systems compared to the traditional payment method in

terms of the older adults, the efficiency, the predictability and the

simplicity of the daily tasks are preferred more, so any system called as

time-consuming will negatively affect the confidence and trust of the older

individual Saha and Kiran (2022), Jiang and et al. (2021). For a lot of seniors who

do not have experience with digital skills, as they typically require

experience in other skillsets, such as application installation and navigation

in setup menus, authenticating banks, and error troubleshooting Lisan (2021), Isa et al. (2022). Literatures show that if consumers

perceive the need to commit additional time to new technologies, their

perceived value will drop, and hence they will distrust the convenience and

reliability of the systems Al-Saedi

et al. (2020), Dhiman

et al. (2020). A new source of risk in time ensues when

even mobile payment interfaces are infiltrated with various forms of

verification and biometric prompts paired with security updates that could be

perceived as superfluous or confusing to our elderly population Anshari

et al. (2021), Nguyen et al. (2022).

Elderly people in general are less tolerant of learning through trial and

error, and they will not engage with technology that is first perceived to take

time Chauhan et al. (2022), George

and Sunny. (2021). Fears about slow transaction processing,

system outages or the need to reset passwords or follow complicated procedures

for recovering lost data increase the lack of trust and discourage the

willingness to use electronic solutions. In the financial transaction process,

seniors like the convenience and confidence in trust and any perceived

inefficiency ruins their confidence in mobile payment channels Hameed and Nigam (2022), Lu

and Kosim (2022). Senior consumers are more ready to trust technologies

that include durability and effectiveness, and are completely functional from

the beginning.

3.4. Perceived Psychological Risk and Trust

Perceived psychological risk comprises the psychological stress, tension, and cognitive uneasiness experienced by humans as they deal with the new technology. The octogenarian is often afraid, confused and worried about committing irreversible mistakes because they are surrounded by technological surroundings which is very likely to provoke embarrassment or incompetence to the octogenarian Hoque and Sorwar (2017), Huang and Chang (2020). Older people are more susceptible to stressors related to usability due to the decreased speed and level of confidence in the use of digital solutions, which leaves them more susceptible to adopting a psychologically uncomfortable stance when it comes to adopting technology Andalib and Hashim (2018), Isa et al. (2022). Though for younger users to understand error-trial learning as a digital interaction mode, the elderly adults often assign social stigmas, financial losses, or lack of control as the cause of digital errors Olsson et al. (2019), Sun et al. (2020). Multi-step navigation, no clarity of route being followed, leads to complications with transactions, and high complexity of transaction process creates psychological risk, and scepticism towards digital payments Cham et al. (2021), Senali et al. (2022). This psychological unfeasibility results in loss of trust and impedes the elderly users' involvement in the digital transaction, leading them with the preference of the traditional face-to-face financial interaction Shankar et al. (2020), Savic and Pesterac (2019).

Psychological risk, overwhelming experience or cognitive burden imposed by digital platforms, such experiences oppose technology adoption Jena (2022a), Tandon et al. (2018). Potential cybercrimes and anecdotal occurrences of fraud across the media, the problem of ambiguity feeds into people's anxiousness and prevents people from experimenting Kamboj and Joshi (2021), Choi and Choi, (2017).

3.5. Perceived Privacy Risk and Trust

This perceived threat to privacy only causes a fear of unauthorised access, misappropriation or disclosure of one's personal and financial information. The problem is especially relevant for ageing because elderly individuals have a poor awareness towards digital safety and cybersecurity threats or risks Chawla and Joshi (2019), Nguyen (2018). Older persons place a high value on data privacy, and these individuals regard digital environments as grey areas where personal data is used without their knowledge Hoque and Sorwar (2017), Wong and Mohamed (2021). The literature shows that privacy breach has significant adverse effect on the trust of the mobile finance system Abouzid et al. (2021), Talwar et al. (2020). In addition, older adults are extremely vulnerable to the effects of identity theft, phishing attacks, and unauthorised withdrawals, and, therefore, do not trust the electronic environment Alghamdi and Basahel (2021), Mutimukwe et al. (2020). Privacy appointment is also higher in areas or communities with a high rate of incidence of digital scam or knowledge about consumer protection, and the elderly are often given advice based only on anecdotal information given by others or the media Khalilzadeh et al. (2017), Rasche et al. (2018). The elderly customers, however, choose physical banking because they feel more control and security in physical banking due to a lack of trust Bhatt and Mehta (2020), Nguyen et al. (2022). Lack of credibility on a particular application in the manner by which the data is stored, the financial information is secured, and the access to the user data has contributed to the reluctance to embrace mobile payments Chang et al. (2021), Ozturk et al. (2017).

3.6. Customer Intent to Buy and Customer Trust

Trust is considered to be a significant predictor of consumer behavioural intention in the adoption of digital payments, especially for the elderly group, who are naturally paranoid of new and unknown technology Talwar et al. (2020), Zhao and Bacao (2021). Trust narrows the digital divide between the different age groups and is a psychological protection mechanism for senior surfers Shareef et al. (2021), Isa et al. (2022). Moreover, the elderly are known to be more tolerant and receptive of mobile payment systems since they would put more trust in institutions like banks, technology providers and regulators Singh and Srivastava (2020), Wong and Mohamed (2021). Trust is believed to bring about early adoption by alleviating certain perceived privacy and security risks, psychological discomfort, and time commitment requirements of adoption Nguyen et al. (2022), Sleiman et al. (2022). In contrast, trust is another alternative to knowledge (for old users, many of whom are digital neophytes) Cham et al. (2021), Choudrie et al. (2018), and which may not need to be competent in a specific area to be comfortable with it. In addition to the behavioural intention, there is also a relationship between the behavioural intention and the behavioural performance, and the larger the trust value is, the higher the behavioural intention, acceptance and habit formation.

Technological advancements are everywhere, yet sometimes trust is a rudimentary part of their adoption. On the other hand, a trusted environment may cause the seniors to be tolerant of light usability problems Savic and Pesterac, (2019), Aslam et al. (2022). For this reason, trust-building activities like transparent communication, easy and secure authentication processes for seniors, as well as specific awareness and support campaigns, should be a focus for financial and fintech institutions. Finally, trust building is a crucial process to engage the older persons in a digital financial ecosystem. The following hypothesis are made based on the review are as follows:

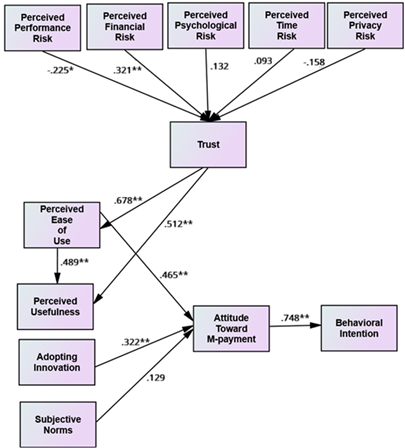

· H1: Perceived performance risk is an important predicting variable of trust in mobile payment adoption by the older people.

· H2: Perceived financial risk is found to have significant impact on trust of older persons in using mobile payment.

· H3: Perceived Time Risk influences the m-payment adoption of the older citizens.

· H4: Psychological risk perception is an important predicting variable of mobile payment practice adoption intention for elderly users.

· H5: The privacy risk perceived by elderly consumer has an impact on the perceived trust in mobile payments adoption.

· H6: Trust positively affects the Behavioural Intention of adopting mobile payment of older people.

3.7. Mobile Payments and Older Adults

The

global phenomenon of the digital payments revolution has been accelerated since

the pandemic and it has convincingly established itself as an important

facilitator of financial empowerment, financial inclusion, and convenience Lu and Kosim (2022), Talwar

et al. (2020). Technological development is run at a fast pace; age

differences in adoption rates are very evident, with a slow pace of

technological adoption and higher perceived barriers among the elderly Olsson et al. (2019), Seifert

(2020). The demographic gap is immense as the aging population growth in

the world is likely to see older people play a major role as economic actors

and payers Benu (2023), Ghilarducci (2022). Accessibility: Not everyone

has the same access to technology: The elderly is structurally and cognitively

disadvantaged, and they have emotional obstacles to adopting financial

technology. Some of these factors include the lack of digital literacy, fear of

technology, fear of cognitive load, risk abhorrence, and low level of

familiarity with mobile phone-based banking systems Hoque and Sorwar (2017), Isa et al. (2022). The emerging trend towards using digital

infrastructures for entirely cashless transactions seems to run the risk of

intensifying digital and financial exclusion without a better understanding of

the behavior of older users Choudrie et al. (2018),

Sun et al. (2020). With continuous evolution

in digital ecosystem, there is need for research emphasizing the psychological,

usability, social, and trust elements that affect the mobile payment uptake

among older persons to achieve economic inclusion Jena

(2022), Saha and Kiran (2022).

The

vital role of trust, perceived ease of use, and perceived usefulness in

generating technology acceptance behaviours in older age Wong and Mohamed (2021), Singh

and Srivastava (2020). Unlike their younger counterparts who adopt

new technologies due to their novelty or long-standing habit, older consumers

are more concerned about dangerousness, system reliability, utility and

cognitive load Cheng et al. (2021), Chawla

and Joshi (2019). Also, the tendency for older adults to adopt

digital payment increases significantly as social institutions and platforms,

such as family, friends, and financial institutions, popularize the benefits

and safety of mobile payment options Shareef

et al. (2021), Santosa et al. (2021).

The conceptual model developed in this study integrates the critical constructs

trust, perceived ease of use (PEOU), perceived usefulness (PU), attitude toward

m-payments, innovation adoption, subjective norm and behavioural intention to

explain older people's adoption decisions.

3.8. Trust in the Adoption of Mobile Payments

Trust

is at the root of digital financial behaviour, especially for the groups who

have always been excluded from state of the art technological systems Khalilzadeh et al., (2017), Talwar et al. (2020). The vulnerability of older

people to cybercrime underscores the prominence of the trust perceptions, which

are closely linked to the incidents of online fraud, information leak, system

infiltration, financial abuse and mismanagement Chang

et al. (2021), Savic and Perstac (2019).

In the case of mobile payment, trust minimizes perceived system transparency,

ethical data processing and institutional credibility Giovanis

et al. (2019), Choi and Choi (2017).

The lack of trust would make people be technologically averse, be more

attentive, and that would make them conservatively adopt banking Nguyen et al., (2022), Jalil

et al., (2022). Trust is another factor that adds to the platform

perceptions exerting on the general cognitive assumptions regarding ease of

learning, reliability, and utility Al-Saedi

et al. (2020) and Saha and Kiran (2022).

It has been found that trust reduces the negative perceptions held by the older

generations towards the technology, especially when systems are perceived as

reliable, user-centric and transparent Wong and Mohamed (2021), Shareef

et al. (2021). Finally, trust is used by elderly people as

the psychological foundation to consider compatibility between the adoption of

mobile payment and financial comfort, subjective value and cognitive ability.

3.9. Perceived Ease of Use (PEOU)

PEOU

is the consumer's perception of how easy it is to obtain knowledge and how easy

it is to utilise mobile payment systems. Elder people also face the same

convenience in adoption because of the decline of working memory, motor

agility, and information processing speed due to old age Choudrie et al. (2018), Sun

et al. (2020). The digital systems' interface can evoke anxiety,

frustration or disconnectedness from digital services Tsai

et al., (2020), Sharma

et al. (2017). The user experience capability features that

are particularly useful for seniors included ease of menu navigation,

navigating and minimising required steps, which are found to significantly

increase the adoption rate Anshari

et al. (2021), Isa et al. (2022). The ambient emotional conditions provided to

the elderly by smart systems have a conducive outcome and increase their

receptivity for learning and trust Singh

and Srivastava (2020), Chawla

and Joshi (2019). Further, it is known to indirectly affect

cognitive evaluation processes by moderating perceived usefulness, where the

more complicated the system is, the less likely it would be perceived as useful

and the less it would lead to an increase in adoption intentions Kamboj

and Joshi (2021), Tan and Chan (2018). As regards the potential challenges of older

consumers, simplicity mitigates the fear of technological failure, loss of

independence, and digital confusion Khasawneh and

Irshaidat, (2017), Chauhan et al., (2022).

3.10. Perceived Usefulness (PU)

Perceived

Usefulness refers to how much older people perceive that the use of mobile

payment systems will improve the efficiency, convenience and reliability of

their day-to-day financial transactions. With increasing age, due to mobility

limitation, health issues and an increase in the need for transactions that

take place from a distance, perceived usefulness of digital solutions increases

Nguyen et al. (2022), Raza et al. (2021). Older users buy favourable

utility assessment because they experience the reduction of physical bank

visits, the dependence on using currency and fast and safe transactions Hoque and Sorwar (2017), Sun et al. (2020).

Usefulness serves an emotional function in the sense of encouraging the

feelings of autonomous and competent self in elderly people who are usually

concerned about their physical incapacity and needing to be cared for by

caretakers or family members Saha and Kiran (2022),

Choudrie et al (2018). This psychological

empowerment is reflected in a greater level of technological confidence and,

hence, greater acceptance.

Perceived

utility is especially important in a demography that was used to conventional

cash-based or face-to-face banking processes for several decades Widyanto

et al. (2022). For many seniors, mobile payments are not just

switching to the new technology; it is switching to a new way of life. As a

result, there is a need to demonstrate a clear practical value in order to get

uptake to take place. Significant cost saving, enhanced security of the

transaction, time saving, and greater control of the financial records

encourage perceived utility and behavioural change Wong and Mohamed (2021), Makanyeza (2017).

On the other hand, low perceived usefulness can be a major inhibitor of

adoption. If elderly people do not have the perception that mobile payments

offer an additional value over existing banking systems, then they are no more

willing to use mobile payments Singh

and Srivastava (2020). The absence of perceived value is often

accompanied by both routines of practice, fear of making digital mistakes and

fear of fraud.

Trust

is also positively correlated with perceived usefulness. Older users tend to

trust those technologies that they find beneficial and trustworthy, which means

that perceived usefulness has an indirect effect on trust in the platform Widyanto

et al. (2022), Wong and Mohamed (2021). When older people notice positive experiences

with a technology that enables them to make transactions in a reliable, safe

and error-free manner, trust is built. On the other hand, poorly perceived or

poorly communicated benefits cause uncertainty, which inhibits experimentation

and inspires avoidance. In conclusion, Perceived Usefulness is a major

framework for evaluation in which seniors measure the introduction of mobile

payments in their daily financial behaviour. The authors suggest promoting transparency

and benefits-oriented adoption rates, as well as ensuring greater focus on

practical use, can work in increasing m-payment utilisation amongst older

consumers.

3.11. Attitude Toward Mobile Payment

Attitude

is a positive or negative perception by the individual towards mobile payments,

according to the perception of benefits of the system, usability and security.

For the older adults, attitude is the result of cognitive assessment (utility,

reliability, simplicity) and emotional comfort with technology Cham et al. (2021), Savic

and Peseterac (2019), Kuo (2020)

suggested that older people make decisions according to their own personal

knowledge, the impact of friends and their own sense of security and

familiarity Shareef

et al. (2021).

The

acceptance of mobile payments among seniors is a progression, involving all

stages: curiosity, experimentation, comfort, habit and attitude, which plays a

central role at all of the stages Al-Saedi

et al. (2020). The positive attitudes have a positive

influence on the desire to explore the world, and the negative emotion states

(i.e., fear, confusion, distrust) have a negative influence on the adoption

process Talwar et al. (2020). Trust and

perceived utility are the main factors to make a positive attitude, as elderly

people have to be assured that the system is beneficial and safe Saha and Kiran (2022), Choudrie

et al. (2018).

Senior

individuals often experience more nervousness and complexity during their

engagement with digital systems. On the other hand, the fear of technological

loss (e.g. loss of money accidentally) as well as mistakes operated by a click

or scamming individuals have the potential to overwhelm the rational benefits

of technology unless they are addressed Choi and

Choi (2017), Savic and Peserac (2019).

Confidence created by previous good experiences leads to positive attitudes and

creates confidence towards digital financial services through a good user

interface and customer support systems. Older adults are more likely to form

their own positive attitudes when their family members or counterparts are seen

engaged in making effective use of the online payment systems, if institutional

communication (e.g., banks, government) help to increase their confidence (see Sharma and Chu (2021) Trusted networks can change

the perception and speed up the adoption in collectivist or close-knit groups Santosa et al. (2021), Nguyen

et al., (2022).

However,

the attitudes can be obstructed by usability problems during the installation

of the hardware for older people. Based on the literature, difficult

navigation, absence of clear instructions, poor local language support, or

support alternatives may generate dissatisfaction and eventually result in

negative attitudes Saha and Kiran (2022), Talwar et al. (2020). As older individuals tend to

place a higher value on the certainty derived from emotions compared to younger

generations, family tech support (speaking to elder members and attending a

bank workshop) and physical help (bank workshops) were found to be important to

influence attitude.

3.12. Behavioural Intention to Adopt Mobile Payments

Behavioural

Intention contains information, attitude and acceptance of the cognitive

opinion of adopting mobile payment methods. In the case of older people,

intention is based on the perceived degree of utility, ease, and

trustworthiness, and positive emotional experience versus negative emotional

experience balance. When the system gives the elderly confidence, value, and

trust, they will be motivated to have strong behavioural intention (Majumdar and Pujari (2022), Jiang et al. (2021). For older consumers,

intention to consume does not directly lead to realising that behaviour unless

the cognitive barriers are eliminated and the confidence is kept intact Tan and Chan (2018), Savic and

Peseterac (2019). Whereas much noise is made as the elders explain their

intentions, they may be hesitant to act on them in practice due to lack of

knowledge or fear of making mistakes Nguyen et al.,

(2022), Osei and Mishra (2022). For

this reason, safety reinforcement, continuous exposure and individual support

are needed for the acquisition of intention. That is even more so when it comes

to trust. Apart from high utility, purpose is less valuable when people have

low trust Singh

and Srivastava (2020), Santosa et al. (2021).

On the other hand, trust in the platform and institutions that support the

older persons would increase and be translated toward increasingly stronger

intention and thus usage Majumdar and Pujari (2022),

Nguyen et al. (2022). Therefore, trust

becomes a psychological barrier and also an emotion.

Older

consumers were more likely to know and use digital payments to make

transactions if they were considered to be mainstream, very well known, and

bank and government-recommended Al-Saedi

et al. (2020), Raza et al. (2021).

On the other hand, negative social stories (e.g., pages reporting cybercrime or

failed electronic transactions) may reduce intention Talwar,

Haldari, Samarthya, and Pradabrata (2020). In conclusion, purpose seems

to be an intrinsic readiness of older people to adopt digital finance, from

reliance on trust, emotional safety and some showcased payoff. Additionally,

rewards for physical activity trials in the form of step counts and efforts,

including a structured onboarding process and social success stories to

encourage and ease the adoption process for seniors, may work better.

3.13. Subjective Norms

Subjective

norms are the feeling of social pressure or motivation to use mobile payment

methods. Older persons are deeply touched by their relational ecosystem with

their family, caregivers, friends, and institutional stakeholders Wong and Mohamed (2021), Shareef

et al. (2021). Family members, especially the younger

generation, are the common technological mentors who help the seniors to

download an application, connect to the bank and practice the transaction Santosa et al. (2021), Nguyen

et al. (2022). Social support helps to reduce fear, increase confidence,

and alleviate the adoption Darma

and Noviana (2020), Alghamdi

and Basahel (2021). In cultures whose adults use family-based

networks a lot for technology guidance, the power of subjective standards is

more powerful. In the case where digital payments are considered as a societal

norm, it is easier for older adults to get accustomed to the habit Tan and Chan (2018), Olsson et al. (2019).

Institutional endorsements are important; seniors believe in banks, governments

and community organisations that advocate and stand up for safe web behaviours Shareef

et al. (2021), Wong and Mohamed (2021). Campaigns targeted at senior demos, like

step-by-step manuals, in-branch teaching or community seminars, are designed to

supplement the propensity to adopt.

3.14. Adoption of Technology Innovation

Technology

adoption is the propensity of an individual to explore new ideas and adopt new

frameworks that s/he is unfamiliar with. Although older persons are slower in

adopting novelty, due to their pre-existing habits and also because they become

even more risk-averse, innovation-minded seniors have an interest in

experimenting Berg and Liljedal (2022), Jena

(2022). Their inquisitiveness, flexibility and

aspiration to keep themselves updated make the digital experiences better Santosa et al. (2021), Tripathi

et al. (2022). Progressive elders are viewing the digital

changes as opportunities rather than threats. They make use of trial and error

learning, spend patience on new systems and make adaptations with new

interfaces Tandon et al. (2020), Fan et al. (2022). Innovation preparedness also enhances

resilience to the transitory challenges, and therefore, diminishes early

desertion of mobile payment platforms. This characteristic has further

interactions with various additional cognitive beliefs. Innovative persons

think about technologies as more user-friendly, useful, and much less harmful Cham et al. (2021), Soh

et al. (2020). As a result, innovation has the benefit of improving

acceptance and, at the same time, strengthening trust and mental readiness. On

the other hand, seniors who have a low attitude towards innovation might

completely avoid digital products altogether. Such persons need organised

support, custom communication and even practical support to overcome

reluctance. Adoption might only take place if simplicity, trust and strong

social reinforcement are involved.

Based

on the above review, the hypotheses are derived as follows;

·

H7:

Trust has a favourable effect on the PEOU of mobile payment systems for senior

citizens.

·

H8:

The PEOU has a positive influence on the PU in the adoption of mobile payment

among senior citizens.

·

H9:

The PU has a positive influence towards attitudes towards the utilisation of

Mobile payment by old persons.

·

H10:

The attitude towards mobile payment positively affects the behavioural

intention to use mobile payment systems for the case of older persons.

4. Materials and

Methods

This

study was based on quantitative and cross-sectional research method to analyze

the factors having an impact on the acceptance of mobile payments by older

persons. The study adopts the TAM and UTAUT model and augmented with the

conceptions of trust and perceived risk aimed to experimentation test the

linkages that influences the behavioural intention towards mobile payment.

Primary and structured survey was used as the primary instrument of data

collection and SEM method is used to conduct efficacy testing of the instrument

in exploring complex causal relationships and establishing latent structures in

the model as used in technology adoption studies. The sample comprised 326

elderly of age group 55 and above who lived in Delhi-NCR region of India. This

area is the domain of a fast expanding urban conglomerate witnessing an

explosion of digital financial inclusion and integration of technology. Due to

difficulty in accessibility and to come close to a wide population of senior

individuals, convenience and snowball sampling techniques were applied. Initial

participants were recruited through senior citizen organizations, community

organizations, residential welfare societies, and through informal networks and

asked for referral of their peers who would meet the study criteria. This split

sample technique enabled participation into the study from the digital active

elderly as well as those gestations their exploration of mobile payment

services.

The

participants were age of 55 years or above, residing in Delhi-NCR and should

have basic knowledge on mobile payment platforms such as Paytm, Google pay,

Phonepe, BHIM-UPI or mobile banking apps have been considered for current study

whereas those who are not using any type of online banking activity have not

been taken into consideration. Researchers with severe cognitive impairment and

no history of using a smart phone were also excluded for clarity of

understanding and substantive engagement. The observations of respondents

consisted of validated scale items were based on the results of other studies

of TAM, UTAUT, trust and risk characteristics with a five-point Likert scale.

Data was collected through scheduled questionnaires given to people in different

commercial offices during their lunch time and residential complexes during

evening time. The questionnaire with extreme values, missing values and having

more than 10% outskirts were discarded during final data analysis process.

Thereafter, responses were evaluated regarding their completeness and

consistency and subjected for statistical evaluation using SEM. Construct

reliability, convergent and discriminant validity and model fit measures were

used to validate the robustness of the findings. This analytical approach

helped a deep in-depth evaluation of the psychological and a functional factors

impacting on digital payment taking of older persons.

5. Results

A

total of 326 older men and women were recruited (nearly equally male and female

respondents). The age of the respondents ranged between 55 and 82 years with an

average age of 62.3 years (surveying both the “young-old” and “old-old”

generations). Level of formal education recorded was very individual within the

sample ranging from people with little to no formal education to those who have

obtained post-graduate qualifications and, therefore, reflects a diversity of

digital and cognitive capacity on how technology is used in later life. The

respondents reported that despite the fact the national trend in using digital

financial services has been rising through the increase in the number of

platforms with UPI, the overall penetration of mobile payment services was

moderate. Forty percent of the respondents said they had previously used

digital payment apps. Out of this sub-segment, the most popular channels were

Google Pay, PhonePe and Paytm. However, a sizable proportion of elderly

respondents who did not go through digital transactions still expressed that

the technology was too complicated, exposed them to a security breach, and they

did not trust the platform. These descriptive tendencies point to the need to

pay close attention to matters of usability and confidence among the increasing

population of older people in the emerging digital economy of India.

All

latent constructs demonstrated factor loadings surpassing the prescribed

minimal limits, Composite Reliability metrics indicated adequate internal

consistency, and Average Variance The extracted values validated convergent

validity. Furthermore, the Variance Inflation Factor values were much below the

permissible upper thresholds, signifying the absence of multicollinearity

issues. The Standardized Root Mean Square Residual (SRMR) value conformed to

specified requirements, affirming the structural integrity of the measurement

model. Collectively, these findings validate the robustness of the survey

instrument and the dependability of the utilized constructs. The demographic

diversity of the sample, along with robust measurement diagnostics, establishes

a rigorous empirical foundation for later structural modelling and hypothesis

testing. This study provides a reliable and contextually relevant analysis of

m-payment acceptance trends among older persons in an urban, technologically

evolving Indian environment.

Table 1

|

Table 1 Profiling of Factors of M-Payment Adoption Among Senior Citizens |

|||||

|

Sr. No. |

Name of Factor |

No. of Items |

Cronbach’s Alpha (α) |

Eigen value |

Factor Loadings |

|

1 |

Perceived Usefulness (PU) |

3 |

0.886 |

3.79 |

PU2 = .889, PU3 = .847, PU1 = .834 |

|

2 |

Perceived Ease of Use (PEOU) |

4 |

0.879 |

3.61 |

PEOU2 = .894, PEOU4 = .862, PEOU1 = .828, PEOU3 =

.781 |

|

3 |

Attitude Toward M-payment (ATT) |

3 |

0.891 |

3.26 |

ATT2 = .904, ATT3 = .872, ATT1 = .823 |

|

4 |

Behavioral Intention (BI) |

4 |

0.876 |

3.15 |

BI4 = .888, BI2 = .854, BI3 = .831, BI1 = .799 |

|

5 |

Subjective Norms (SN) |

3 |

0.843 |

2.89 |

SN3 = .868, SN1 = .841, SN2 = .793 |

|

6 |

Image (IMG) |

4 |

0.825 |

2.74 |

IMG4 = .851, IMG1 = .828, IMG3 = .804, IMG2 =

.776 |

|

7 |

Trust (TR) |

5 |

0.911 |

3.98 |

TR5 = .924, TR3 = .897, TR1 = .875, TR4 = .862,

TR2 = .829 |

|

8 |

Perceived Privacy Risk (PPR) |

3 |

0.868 |

2.83 |

PPR2 = .889, PPR3 = .861, PPR1 = .822 |

|

9 |

Perceived Performance Risk (PFR) |

4 |

0.854 |

2.95 |

PFR3 = .871, PFR4 = .838, PFR1 = .815, PFR2 =

.781 |

|

10 |

Perceived Financial Risk (PFRN) |

4 |

0.882 |

3.02 |

PFRN1 = .893, PFRN4 = .871, PFRN3 = .848, PFRN2 =

.796 |

|

11 |

Perceived Psychological Risk (PSYR) |

3 |

0.852 |

2.88 |

PSYR3 = .879, PSYR1 = .841, PSYR2 = .802 |

|

12 |

Perceived Time Risk (PTR) |

3 |

0.845 |

2.73 |

PTR1 = .854, PTR3 = .826, PTR2 = .791 |

|

Source Primary Data (SPSS 23.0

Version) |

|||||

The

factor analysis was conducted in order to determine the statistical correctness

of the model in m-payment adoption. This technique was helpful in testing item

clustering, factor integrity and psychometric robustness of the measures using

frameworks on technology adoption and risk perceptions. The sampling adequacy

was confirmed with a KMO score of 0.886 which means that adequacy of the

dataset for the extraction of factors, whereas the significant results of

Bartlett’s Test of Sphericity (χ² = 5012.48, p < 0.001) showed that

there were appropriate correlation relationships among the variables and the

methodology of the factor analysis method was appropriate Hair et al. (2017). The total variance explained of 72.4%

represented a considerable portion of the underlying behavioural and

psychological characteristics of relevance to acceptance of mobile payments.

The reliability analysis showed that the values of Cronbach’s alpha ranging

from 0.825 to 0.911 indicated good internal consistency. Favourable reliability

had been reported for the constructs that measure trust (α = 0.911),

attitude toward m-payments (α = 0.891) and perceived financial risk

(α = 0.882) which shows coherence, and consistency among the questions

related to these dimensions. The various risk factors, such as privacy,

performance, financial, psychological and time risk factors, were showed

significant explanatory relevance, thus making them valid to validate their

theoretical relevance in the analysis of senior’s resistance towards the

m-payment systems.

In

addition, the issue of item loadings was demonstrated by factor loadings for

which all greater than 0.70, showing the adequate convergence of items and thus

their appropriate representation of each construct. This pattern forms a check

that the pattern of the measurement items was successfully associated with

their corresponding latent variables and the item was found to make a

significant contribution to the factor solution. The results of EFA are used to

assure the reliability and validity of the tool of measurement and this results

in applying further structural modelling to test strong hypotheses about the

factors that determine m-payment adoption behaviour among older persons.

Table 2

|

Table 2 Final Results of Measurement Model of M-Adoption of Proposed and Final Model |

||||||

|

Proposed Model |

Final Model |

|||||

|

Constructs |

CR |

AVE |

ASV |

CR |

AVE |

ASV |

|

Perceived Usefulness (PU) |

0.874 |

0.661 |

0.428 |

0.911 |

0.721 |

0.392 |

|

Perceived Ease of Use (PEOU) |

0.861 |

0.642 |

0.412 |

0.887 |

0.665 |

0.377 |

|

Attitude Toward M-payment (ATT) |

0.883 |

0.701 |

0.455 |

0.904 |

0.758 |

0.423 |

|

Behavioural Intention (BI) |

0.862 |

0.684 |

0.462 |

0.895 |

0.739 |

0.436 |

|

Subjective Norms (SN) |

0.842 |

0.584 |

0.378 |

0.869 |

0.627 |

0.344 |

|

Image (IMG) |

0.827 |

0.601 |

0.389 |

0.854 |

0.662 |

0.352 |

|

Trust (TR) |

0.884 |

0.693 |

0.436 |

0.917 |

0.734 |

0.401 |

|

Perceived Privacy Risk (PPR) |

0.852 |

0.669 |

0.414 |

0.883 |

0.716 |

0.387 |

|

Perceived Performance Risk (PFR) |

0.837 |

0.642 |

0.391 |

0.867 |

0.688 |

0.362 |

|

Perceived Financial Risk (PFRN) |

0.865 |

0.681 |

0.422 |

0.894 |

0.713 |

0.398 |

|

Perceived Psychological Risk (PSYR) |

0.844 |

0.652 |

0.406 |

0.876 |

0.701 |

0.379 |

|

Perceived Time Risk (PTR) |

0.836 |

0.637 |

0.388 |

0.869 |

0.688 |

0.351 |

|

Source Primary Data (AMOS 23.0

Version) (Composite Reliability (CR),

Average Variance Extracted (AVE) and Average Shared Variance (ASV) |

||||||

All

indicators of the model indicated acceptable standardized loadings, which

varied between 0.70 and 0.912, which is higher than the threshold of 0.70 which

is recognised as satisfactory. This was used to make sure that all items were

making significant contributions to the latent construct, and were meeting

indicator reliability criteria for the model. He psychometric validity of

measuring model was investigated, based on CR, AVE and ASV, by studying the

internal consistency, convergent validity and the discriminant validity. In

both the models namely the preliminary and the modified models, the CR values

were always greater than 0.70 which suggested good internal reliability. The

result of the refined model was higher CR scores for key constructs (perceived

utility, attitude, and trust), indicating that the refinishing process (i.e.,

item deletion and elaboration/re-specification) helped to improve measurement

construct clarity and accuracy. The AVE values that were all greater than 0.50

for all constructs implied that the modified ones better represented the

variations mapped on their base theoretical constructs, and increasing

construct coherence accordingly. In the improved model the lower values of ASV

was an indicative that there is good discriminative validity.

Based

on the Fornell-Larcker criteria, AVE values for all constructs were higher than

ASV values, indicating that latent variables were capturing more variance with

respective indicators as compared with variances with other constructs in the

model. The psychometrical strength of the better measuring model was better

than that of the measuring models in the other two categories of fit. CR, AVE

and ASV with an improvement of the measurement instrument as proof of

conclusive evidences for the reliability and validity of measurement

instrument. This study contributes to increase the trust of structural analysis

in the future and increases the methodological validity of the findings of the

study drawn from the study in terms of the response m-payment uptake by the

elderly.

Table 3

|

Table 3 Fornell-Larcker criteria of Measurement Model of M-Adoption |

||||||||||||

|

Constructs |

PU |

PEOU |

ATT |

BI |

SN |

IMG |

TR |

PPR |

PFR |

PFRN |

PSYR |

PTR |

|

PU |

.849 |

|||||||||||

|

PEOU |

.618 |

.815 |

||||||||||

|

ATT |

.634 |

.601 |

.871 |

|||||||||

|

BI |

.552 |

.537 |

.693 |

.86 |

||||||||

|

SN |

.428 |

.412 |

.503 |

.526 |

.833 |

|||||||

|

IMG |

.482 |

.465 |

.519 |

.544 |

.567 |

.814 |

||||||

|

TR |

.574 |

.588 |

.607 |

.619 |

.466 |

.541 |

.857 |

|||||

|

PPR |

-.372 |

-.364 |

-.398 |

-.385 |

-.351 |

-.363 |

-.402 |

.846 |

||||

|

PFR |

-.331 |

-.348 |

-.364 |

-.358 |

-.319 |

-.335 |

-.362 |

.426 |

.829 |

|||

|

PFRN |

-.354 |

-.372 |

-.386 |

-.373 |

-.327 |

-.339 |

-.381 |

.414 |

.453 |

.844 |

||

|

PSYR |

-.318 |

-0.332 |

-.356 |

-.341 |

-.296 |

-.322 |

-.344 |

.401 |

.438 |

.426 |

.837 |

|

|

PTR |

-.292 |

-.309 |

-.321 |

-.337 |

-.283 |

-.301 |

-.329 |

.382 |

.417 |

.404 |

.389 |

.83 |

|

Source Primary Data (AMOS 23.0

Version) |

||||||||||||

Discriminant

validity was measured by the Fornell-Larcker method which requires the square

root of each AVE of the constructs to be higher than their correlation with

other constructs. The results confirmed that this criterion was met. The AVE

values for all constructs was taken by square root were found to be greater

than those of inter-construct correlations. This, in turn, suggests that each

construct had more common variance with its own indicators than did indicators

of other constructs and hence indicating confirmation of discriminant validity.

The overall trend results show that perceived vulnerability lowers confidence

and lessens the possibility of using digital channels of payments. Moreover,

the solid positive correlations among the risk dimensions suggest that older

users often consider risks in a holistic manner; in other words, if older users

are worried about one type of risk, they are frequently too sensitive to the

other types of risk, as well. These results are excellent empirical evidence for

the measurement model discriminant validity. Furthermore, the theoretical

relationships assumed in the conceptual model have been confirmed as the

respective categories were found to reliably represent different and relevant

aspects of mobile payment acceptance and risk perception among older people in

a digital finance system.

Table 4

|

Table 4 CFA Model and Fit Indices of M-Banking Among Senior Citizens |

|||||

|

Fit Index |

Proposed Model |

Final Model |

Fit Index2 |

Proposed Model3 |

Final Model4 |

|

CMIN/DF |

3.482 |

2.413 |

NFI |

0.903 |

0.934 |

|

GFI |

0.894 |

0.935 |

CFI |

0.926 |

0.958 |

|

AGFI |

0.862 |

0.910 |

TLI |

0.918 |

0.951 |

|

RMSEA |

0.079 |

0.054 |

SRMR |

0.084 |

0.071 |

|

Source Primary Data (AMOS 23.0

Version) |

|||||

The

comparison between the baseline structural model and final refined model shows

a major improvement of the overall model fit after the systematic

modifications. The changes made the framework more parsimonious and explanatory

and demonstrated that the re-specification of measurement items and pathways

developed a much more congruent relationship between the postulated structure

and the outcome of the data. A significant improvement in CMIN/DF (from 3.482

to 2.413) suggested to be a desirable level and indicates a more parsimonious

model that is able to explain the data using less residual discrepancies. The

results witnessed significant improvement in both GFI and AGFI values. The

correlation indices in the modified model were both greater than 0.90, indicating

a better agreement with the empirical covariance structure than was found in

the original model. Furthermore, the values of NFI, CFI, TLI found to be more

than 0.9, suggest that the improved model has more explanatory power than the

null model. In addition, better convergence was suggested by absolute fit

indices. The value of RMSEA < 0.08 and SRMR < 0.10 indicated that the

revised model was considered an accurate representation of known relationships

with increased precision and lower residual levels. Together, these

improvements demonstrate that the improved model has a statistically stronger

fit, and also a more reliable and theoretically solid foundation, for

behavioural determinants of mobile payment acceptance among higher-aged consumers.

6. Theoretical

Discussion

This

study is an extension of TAM Model in which perceived risk factors and

perceived trust are introduced as important psychological mechanism. While the

TAM Model mostly consider the usefulness of perceived usefulness and ease of

use with respect to technology adoption Davis (1989),

more socio-psychological factors like increased vulnerability, cognitive

barriers and susceptibility of the presence of trust in digital environment are

critical in the adoption of technology by elderly people Vaportzis et al. (2017). The findings point out

that trust plays a psychological role as the basis of digital payment

decision-making among the older generation, which affects risk perceptions,

attitudes and behavioural intentions.

6.1. Trust as the Key Enabler in Old Digital

Financing

The

results show that trust is an important consideration that influences adoption

process by facilitating higher cognitive assurance and lower technological

uncertainty. Trust is substituted for experience or familiarity and alleviates

fear in fintech industry Gefen et al (2003);

Pavlou (2003). Older people, who are often

digitally less literate and more susceptible to fraud on the internet, trust

institutions and perceptions of trust the most Mitzner

et al. (2019). When reliable, mobile payments are perceived to be

convenient and this leads to positive attitude and intention to adopt, and this

is so in all cases. The trust issue leads to increase if not actual fears of

mistake, deception, and inappropriate use of the system and therefore increased

reluctance and avoidance. This is supported by Kim

et al (2009) who identified trust being an important factor affecting

the adoption of online financial services by e-service unwilling users.

6.2. Perceived Risk and Its Effects Through

Different Sides

These

findings show that older persons estimate that they are vulnerable to being

defrauded, which continues to be an important factor hindering the adoption of

fintech. It is due to their emotional vulnerability that seniors see relatively

low levels of technical disruption as having high levels of loss potential due

to the lack of trust in recovery Barnard et al. (2013)

while younger users are more used to digital operations. This study

carried out five different Risk dimensions and their impact on trust. Perceived

performance risk adversely affected the trust emphasizing the functional

reliability sensitivity among the elders. The expectations of the older age

group in technology are that it functions well and consistently; the

uncertainty towards the stability of the system is what leads to the lack of

trust Lee (2009). Here the potential exists

that the older people have the potential to have lower tolerances of digital

fault durations, troubleshooting, which could lead to a rapid decline in their

trust of failure of performance. The financial risk perceived correlated

positively with trust, which was suggestive of compensating behaviour. The

results are somewhat similar to that of Martins et

al. (2014) in that senior responders that were aware of potential

financial risk factors were more likely to rely on reputable providers and

strong institutional structures. This may imply some form of protective

strategy to building trust and favouring the use of institutions instead of

foregoing technology entirely.

Psychological

threat, which is more conceptually important, was also not significantly

related to trust, suggesting that emotional fear may not be enough to

discourage the development of trust in conjoint with safety assurances and

perceived benefits. Previous work has shown that older people may be disturbed

when learning if it was reassured that the long-term benefits will be positive He et al. (2018). However, psychological pressure

resulting from the fear of errors is still a recognised barrier to the digital

migration Czaja et al. (2006). In addition,

temporal risk did not have a negative effect on trust. The price of deference

in learning time to the digital payment system can be paid back when the

advantages are achieved. This is in contrast to data on younger consumers, who

display a higher time-sensitivity Koenig-Lewis et

al. (2015). In contrast, subjective privacy risk had a significant

negative effect on confidence. The elderly people see too much fear when it

comes to the disclosure of personal information and misuse of data, due to

their lack of cybersecurity knowledge and sense of vulnerability Anderson and Perrin (2017). Consistent with Yang et al. (2015), the media reports and digital

fraud stories exaggerate the risk awareness of the elderly. Hence, privacy

protection and transparency are conditions of importance for building

confidences.

6.3. Technology Acceptance by the Elderly consumers

PEOU

was a significant impact on perceived usefulness and attitude. For older

people, intuitive designs, easier to navigate, voice interaction and working

environments that are better for the eyes are important Mitzner et al. (2019). Majumdar and

Pujari (2022) suggested that easing provides less cognitive fatigue and

improves confidence in learning and develops a positive image. The innovative

propensity positively influenced the attitudes, which means that seniors with

curiosity and psychologic inclination attitudes suppose more active in digital

adoption. The so-called older people are very diverse: there are internet

saviours retirees, and there are those afraid and avoidant Chen and Chan (2014). Relative utility was a

significant influence on the attitudes which means that the elders had positive

attitudes to mobile payments if they perceive that the advantages will assist

them by reducing physical dependence on the bank and providing more autonomy.

The value of perception with lifestyle may overcome resistance Choudrie et al. (2018). It is discovered that

psychological preparedness has a positive impact and further technology

adoption. The application of subjective norms did not cause significant

difference in attitude. This indicates that those aged have less need for

social influence once basic knowledge has been learnt. While social influences,

as demonstrated by Wang et al. (2014) begins

the process, further adoption has to do with the self-assessment, and not

social intelligence, the reverse of the case of young people who are first

showed by their peers when it comes to digital engagement. This difference can

be explained through the autonomy to take one's own decision in later stages of

life, which is shown through older persons.

6.4. Attitudinal and Behavioural Intentions

The

results suggested the significant effect of emotional acceptance on behavior

intention, which implies that emotional acceptance is a precursor of habit

formation. An improvement in the emotional filtering in technological

decision-making have been highlighted by older people that need to have

feelings of confidence, respect and psychological security Quan-Haase et al. (2018). Positive experience has

a positive impact, and perceived control has a positive moderating effect on

the adoption and continuing usage of digital payment systems.

The

findings call for digital banking ecosystems to take into consideration age

inclusive service designs and communication strategies. Service providers hold

the responsibility of emphasizing seamless and error-free interfaces with

supportable processes for fraud prevention while providing opportunities for on

boarding, with human support as well as educational seminars. Key usability

features are increased text, voice guidance and navigation features and are

easy to understand whereas transparency of privacy principles and guaranteed

messaging, on a regular basis, are key for trust-building and confidence in

older consumers. These initiatives are helping to build a safe, supported and

empowered digital payments ecosystem, and allow aged persons to have the

confidence to participate and appreciate in the rapidly changing digital

economy.

6.5. Practical Implications

The

results of this research can provide a myriad of practical information for

legislators, mobile technology providers, financial services and community

organizations that want to accelerate the use of mobile payments by older

adults. For this reason, we stress the importance of development of trust-based

ecosystem since, as the findings revealed, the trust is a significant component

that influences the decisions of adoption of the older users. Older adults

engage in interactions with information systems with a heightened awareness of

risk and vulnerability due to lack of digital literacy, a history of banking

using physical banks, as well as fears of fraud and errors. As a result,

digital payment providers and financial authorities should take a pro-active

approach to establishing trust dependent on transparency, credibility and user

confidence. This has led to clear dispute resolution processes implemented,

clear refund policies, secure authentication mechanisms and clear anti-fraud

message and practices Abouzid

et al. (2021), Giovanis

et al. (2019). Older users will operate more mobile payments

to be psychologically safe, when they perceive more protection.

Older

people tend to need structured and incremental learning processes that are

anxiety reducing and self-efficacy building Olsson

et al. (2019). Some examples of such outreach efforts include

community-based training events, digital literacy workshops held by elder

centres, intergenerational training events, workshops with the help of

show-and-tell sessions conducted jointly with the local banking institutions

and manuals with picture based instructions. Peer to Peer support/tech

assistance (civil society) mediated over phone-lines to minimise technology

phobia, to have the scope for trial and error. Based on the plausibility